Donald Trump’s "King of Debt" Playbook

Reverse-Engineering the American Tax Code to Build an Unfair Business Advantage

For the average worker, debt is a terrifying economic anchor. It is a financial trap paid down slowly with painful, post-tax income. But for the ultra-wealthy, debt is something completely different. It is the premium raw material used to forge corporate empires - and build an impenetrable shield against the IRS.

Love him or hate him, Donald Trump is the ultimate poster child for this parallel financial reality. He even gave himself a bold title: the "King of Debt". While the middle class stays awake at night worrying about paying off their small mortgages, the elite are busy leveraging billions to buy massive, cash-flowing assets.

Here is the truth you need to swallow: debt is not a moral failing. It is a strategic corporate instrument. The entire global financial system is mathematically rigged to reward the people who borrow to build. At the exact same time, it quietly punishes the amateurs who try to save their way to true wealth.

If you want to win this game, you have to stop playing by the rules of the poor and start thinking like a true capitalist. 🏛️🚀

The Art of the Steal: How to Layer a Capital Stack

Let's talk about the ultimate corporate art form: layering a "Capital Stack". The goal here is beautiful in its simplicity. You acquire a controlling stake in a massive, appreciating asset while exposing exactly zero dollars of your own liquid cash. You let other people take the financial risk while you pull all the strings.

Let's look at the history books for a literal masterclass in using Other People's Money. Back in 1976, New York City was teetering on bankruptcy. There was a rundown property called the Commodore Hotel. Trump did not have a massive pile of cash, but he locked down an exclusive option to buy the place for $12 million. How did he fund it? He didn't use his own money. Instead, he engineered a beautiful loop of circular dependency.

First, he convinced the desperate city government to give him an unprecedented 40-year property tax break. That legal guarantee of zero property taxes ended up costing the city over $410 million in lost revenue. But Trump did not just sit on that tax break - he weaponized it. He walked into the Bowery Savings Bank, slapped that $410 million municipal subsidy on the desk, and used it as collateral to force them into giving him a $70 million construction loan.

Then, to satisfy the bank, he brought in the billionaire Pritzker family from the Hyatt Corporation to provide the operational equity and co-guarantee the loan. Finally, his dad tossed in a $1 million loan to backstop the early credit draws. Look at the loop: the city needed a developer to grant the tax break, the bank needed the tax break to grant the loan, and Hyatt needed the loan to commit the equity. By pulling all these levers at the exact same time, Trump walked away with a 50% ownership stake in a massive Manhattan asset without spending a single dollar of his own cash.

In 1979, he pulled off the exact same stunt with Trump Tower. Instead of buying the land outright, he formed a joint venture with the company that already owned the dirt beneath the building. Then they used that institutional weight to secure a massive construction loan from Chase Manhattan Bank.

But the real magic happened decades later in 2012. The tower was highly successful and full of commercial tenants. Trump executed a commercial mortgage refinance for a smooth $100 million. Because bank debt is not taxable income, he walked away with $100 million in completely tax-free cash straight into his pocket. Meanwhile, the tenants in the building paid the rent that serviced the bank's interest. 💸

Here is the translation for your small business: you do not need a billion dollars - and you certainly do not need a rich dad. You just need to stop behaving like a solo grinder and stop using your personal checking account to fund your business growth. Stop asking how much cash you have in your pocket, and start learning how to layer the bank's money to build your empire. 🤝💼

The IRS Illusion: Phantom Expenses and the Near-Billion-Dollar Shield

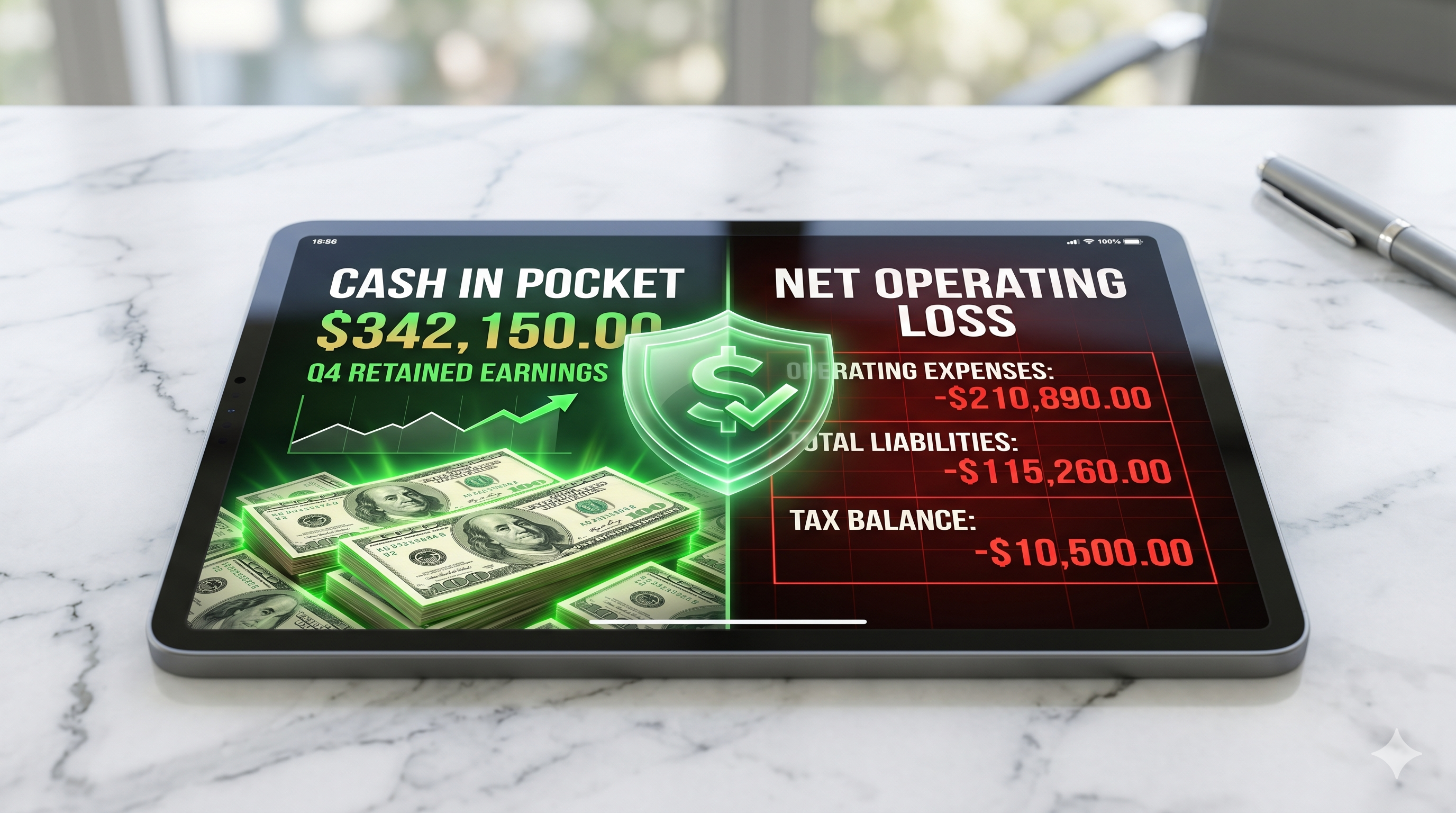

Welcome to the ultimate loophole in the American tax code: debt is completely tax-free, and physical assets allow you to fabricate "phantom expenses". The IRS lets you deduct the imaginary "wear and tear" of a commercial building through depreciation. Smart operators use "cost segregation" to accelerate these deductions into the first few years of owning a business.

The mathematical reality versus the taxable reality is a beautiful illusion. Look at how the math plays out:

You literally pocket $400,000 in pure cash profit, but legally report a $100,000 loss to the IRS. 🤡

This exact strategy is how Trump manufactured his legendary $916 million Net Operating Loss in 1995. When his Atlantic City casinos collapsed into bankruptcy, his lenders forgave over $1.1 billion in debt. Normally, the IRS aggressively taxes forgiven debt as income.

To protect his massive paper losses, his legal team used a brilliant loophole. They stretched a corporate equity exception to cover his partnerships. They swapped practically worthless casino equity for roughly $475 million in canceled debt. Because they legally gamed the system by trading equity instead of cash, the IRS was left completely empty-handed.

By deleting that canceled debt from his taxable ledger, he kept his $916 million loss completely intact. He carried that massive tax shield forward to legally erase his income tax liabilities on nearly a billion dollars of future earnings for almost two decades. That is how you turn a corporate disaster into an absolute masterclass in wealth preservation. 🛡️📈

The Ultimate Calculus: "Buy, Borrow, Die" Applied to You

Amateurs love to save money and sell assets when they need cash. The elite do the exact opposite. They use a strategy called "Buy, Borrow, Die". Let’s look at the brutal math of trying to pull out $1 million in cash from a $3 million portfolio.

If you choose Option A and sell your assets, you hit a massive wall of capital gains taxes. At a combined 33.8% tax rate, you have to liquidate a staggering $1,437,194 just to clear your $1 million cash goal. You instantly hand $437,194 to the IRS, permanently crippling your portfolio's compounding base.

Now look at Option B. Instead of selling, you take out a $1 million line of credit at 6% interest using your portfolio as collateral. Because bank debt is not taxable income, you pocket the full $1 million completely tax-free. Your entire $3 million capital base stays completely intact and continues compounding at an average of 8%. Over a 10-year period, because your asset growth outpaces the interest on your debt, you walk away with a net wealth advantage of exactly $1,311,948 compared to the guy who sold. You are literally being paid to access your own money. 🧠💰

But what about paying back the loan? That is where the "Die" phase comes in. Under Internal Revenue Code Section 1014, the IRS grants a magical loophole called the "stepped-up basis". The exact second your heart stops beating, all your accumulated capital gains are completely erased from the ledger. Your heirs inherit the assets at current market value. They can instantly sell a small fraction completely tax-free, wipe out the bank debt that funded your lifestyle, and absorb the remaining millions without paying a single dime in capital gains tax. 💀🕊️

Now, you probably aren't building a glass skyscraper on Fifth Avenue, but this exact financial architecture belongs in your small business. This is where you shift from a solo grinder to a master of capital. You weaponize 0% Business Credit Stacking.

Instead of waiting until you have a multi-million dollar real estate portfolio to borrow against, you stack $50,000 to $150,000 in revolving, 0% introductory business credit lines. This is your personal version of the elite capital stack. You deploy this interest-free bank money to fund your payroll, scale your marketing funnels, and hire global talent. You keep 100% of your equity, pay zero interest, and let the incoming revenue from your optimized business machine pay down the lines. Stop playing on hard mode with your own wallet. Reverse-engineer the system and let the banks fund your empire. 💳🚀

Buy the Racetrack

The poor use debt as a financial crutch to buy cheap liabilities that keep them trapped on the treadmill. The elite use debt as a high-velocity weapon to acquire massive, cash-flowing assets. It is time for you to choose which side of the ledger you want to live on.

Stop trying to bootstrap your way into a predictable poverty trap. Stop playing this high-stakes game with your own hard-earned money.

It is time to plug directly into the Funding Machine. Secure your 0% introductory war chest and start operating like a true corporate architect. Do not wait for permission from a lazy banker. Head over to 7 Figures Funding right now, claim your free pre-approval, and start building your empire today. 🏛️💳🚀