The Warren Buffett Myth

The Hidden Math Behind the World's Ultimate "Safe" Investor

I love watching the retail finance bros on Twitter.

They all seem to think Warren Buffett got rich by patiently sipping Cherry Coke, reading boring annual reports, and stubbornly "buying and holding" undervalued stocks like the ultimate conservative grandfather of savings.

It’s a great story. It’s also a complete myth. 🤡

Buffett isn't some magical stock picker. He is actually the world's most aggressive, cutthroat insurance salesman. He didn't build the Berkshire Hathaway empire on folksy stock tips; he built it on massive, invisible leverage.

His real cheat code is a little concept called "The Float." Buffett figured out decades ago that if you buy an insurance company like GEICO, millions of people will gladly hand you giant piles of cash today for a service you might not have to provide for three years. He takes that free money, invests it to grow his own empire, keeps 100% of the profits, and pays the claims later.

The elite don't sit around waiting to get paid. They collect cash upfront, invest it for free, and pay it back later. If you actually want to scale your business, you have to stop playing the traditional cash flow game and learn to engineer your own float.

Let's look at the clear math. 🚀

The B2B Slaughterhouse (Why You Are Bleeding Out)

Let’s talk about the absolute worst feeling in business. You just closed a massive contract. Your top-line revenue for the month looks incredible. You are high-fiving your team, updating your CRM, and maybe even popping a bottle to celebrate. 🍾

But then Friday rolls around. You log into your commercial banking app to run payroll, and your stomach drops. The money isn't there.

Why? Because the traditional B2B model is a completely rigged game designed to bleed you dry. You pay for the marketing upfront. You pay your staff upfront. You deliver a world-class service. And then... you sit on your hands and wait.

The global standard for B2B payment terms is a suffocating 45 days. That means you are carrying all the risk, fronting all the capital, and then giving your client a month and a half to casually decide when they feel like paying you while your own bills pile up.

Here is the sick joke: right now, 56% of U.S. small businesses are sitting on an average of $17,500 in unpaid invoices. Let me translate that math for you. You are acting as an involuntary, zero-interest lender to your own clients. 🤡

You are literally financing their empire while starving your own.

In this broken model, growth actually punishes you. The faster you scale, the more cash you burn upfront to deliver the service, and the deeper the hole gets while you wait for those 45-day invoices to finally clear. You are literally getting punished for winning.

This is exactly why a staggering 82% of business failures are caused directly by poor cash flow management. These businesses didn't fail because they had a bad product or lacked ambition. They simply bled to death in plain sight, waiting for a check to clear. 🩸

The GEICO Cheat Code: The Math of Free Money

While you are suffocating, waiting 45 days for a client to finally cut you a check, the "Oracle of Omaha" (Warren Buffett) is playing a completely different sport.

Think about how beautiful the insurance business model actually is compared to your standard B2B setup. In a normal business, you do the work, burn your own capital, and pray you get paid. In the insurance game, millions of people hand you giant piles of cash today for a service you might provide three years from now. And if they never crash their car, you just keep the money.

This massive, revolving pool of collected premiums waiting to pay out claims is called "The Float." And it is the single greatest wealth-building cheat code ever invented.

The Float is billions of dollars of Other People's Money (OPM) just sitting in Buffett's vault. It doesn’t actually belong to him, but he gets to keep 100% of the yield he generates by aggressively investing it while he waits for the claims to come due.

Let’s look at the sheer scale of this invisible leverage. In 1967, Berkshire Hathaway’s float was a cute $18.5 million. By 2025? That number had exploded to a colossal $176 billion. 🤯

That is $176 billion of free capital to buy companies, dominate markets, and aggressively scale, all without diluting his own equity or begging a bank for a loan.

But here is where the math gets genuinely mind-bending. If you or I go to a traditional bank to fund our growth, we are paying 9%, 10%, or maybe 15% in interest. Because Buffett enforces such ruthless underwriting discipline at GEICO and his other insurance holdings, his cost of capital is often negative.

Read that again. Negative.

People are literally paying him to hold and invest their money. Historically, his float has cost him roughly 3% less than what the U.S. government pays to borrow money on risk-free Treasury bills. He borrows capital cheaper than the country that literally prints it! 🖨️💵

Because this money is effectively free and non-callable (meaning a bank can't suddenly panic and demand it back), Buffett comfortably applies a 1.6-to-1 leverage ratio to his investments. The retail finance bros think leverage is incredibly dangerous because they trade on margin and get completely wiped out by margin calls when the market dips. Buffett never gets a margin call because his leverage is brilliantly disguised as insurance premiums.

He isn't a conservative, "safe" grandfather. He is an apex predator swimming in a $176 billion pool of zero-cost capital.

If you want to build an empire, you have to stop playing with your own expensive cash and start manufacturing your own float.

The Tech Titans & The Negative Cash Cycle

Now, I can already hear the excuses. "But Leo, I don't own a massive insurance conglomerate! I can't do that!"

You don't have to sell car insurance to manufacture free money. You just have to reverse your cash flow. Enter the Negative Cash Conversion Cycle (CCC).

Back in 1997, Dell Computer pulled this off by forcing their suppliers to hold all the inventory risk, squeezing out a negative CCC that yielded an annualized working capital savings of over $317 million. But if you want to see the ultimate masterclass in weaponized cash flow, look at Jeff Bezos. 📦

Think back to the 2001 dot-com bloodbath. The market completely crashed. Tech startups were getting vaporized overnight because they burned through their capital and ran out of cash. It was an absolute graveyard. 💀

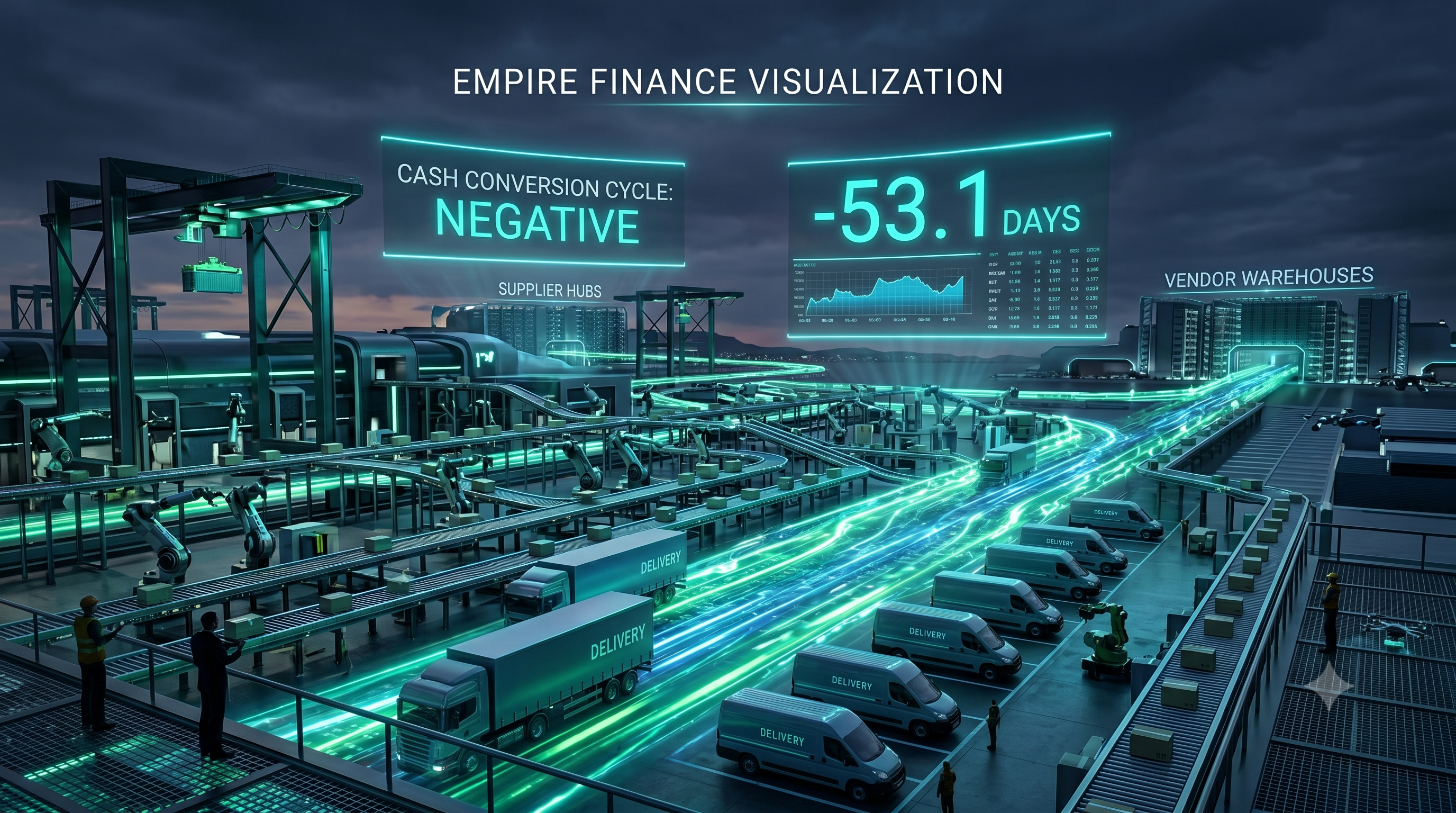

But Amazon didn't just survive; they conquered. Why? Because while everyone else was choking to death, Amazon was operating with a Cash Conversion Cycle of -28.2 days.

Here is how Bezos played the game: When you bought a book or a CD on Amazon in 2001, they charged your credit card instantly. They had the cash in their bank account that exact second. But did they turn around and immediately pay the supplier who actually made the product?

Absolutely not.

Amazon delayed paying their suppliers for an average of 98.6 days.

Let that sink in. They collected cash on day one and legally held it hostage for over three months. They engineered nearly a month of free, liquid cash float on every single transaction. While their competitors were begging traditional banks for expensive loans just to keep the lights on, Amazon was literally forcing its own vendors to fund its survival and explosive growth for free.

And they never stopped. By 2020, Amazon pushed that negative CCC to an insane -53.1 days. 📉

They don’t use their own money to build those massive fulfillment centers. They use the supplier's money. They force the entire global supply chain to act as their personal, 0% interest credit facility.

The elite don't wait to get paid. They take the cash upfront, deploy it to grow, and pay their bills whenever they feel like it.

The Desperation Trap: What NOT To Do

So, you are sitting there choking on that suffocating 45-day wait time for your clients to finally pay you. You aren't Amazon, and you don't own GEICO. You panic. You need cash yesterday just to make payroll.

So, you take a shortcut. You walk right into the slaughterhouse and sign up for a Merchant Cash Advance (MCA). 💀

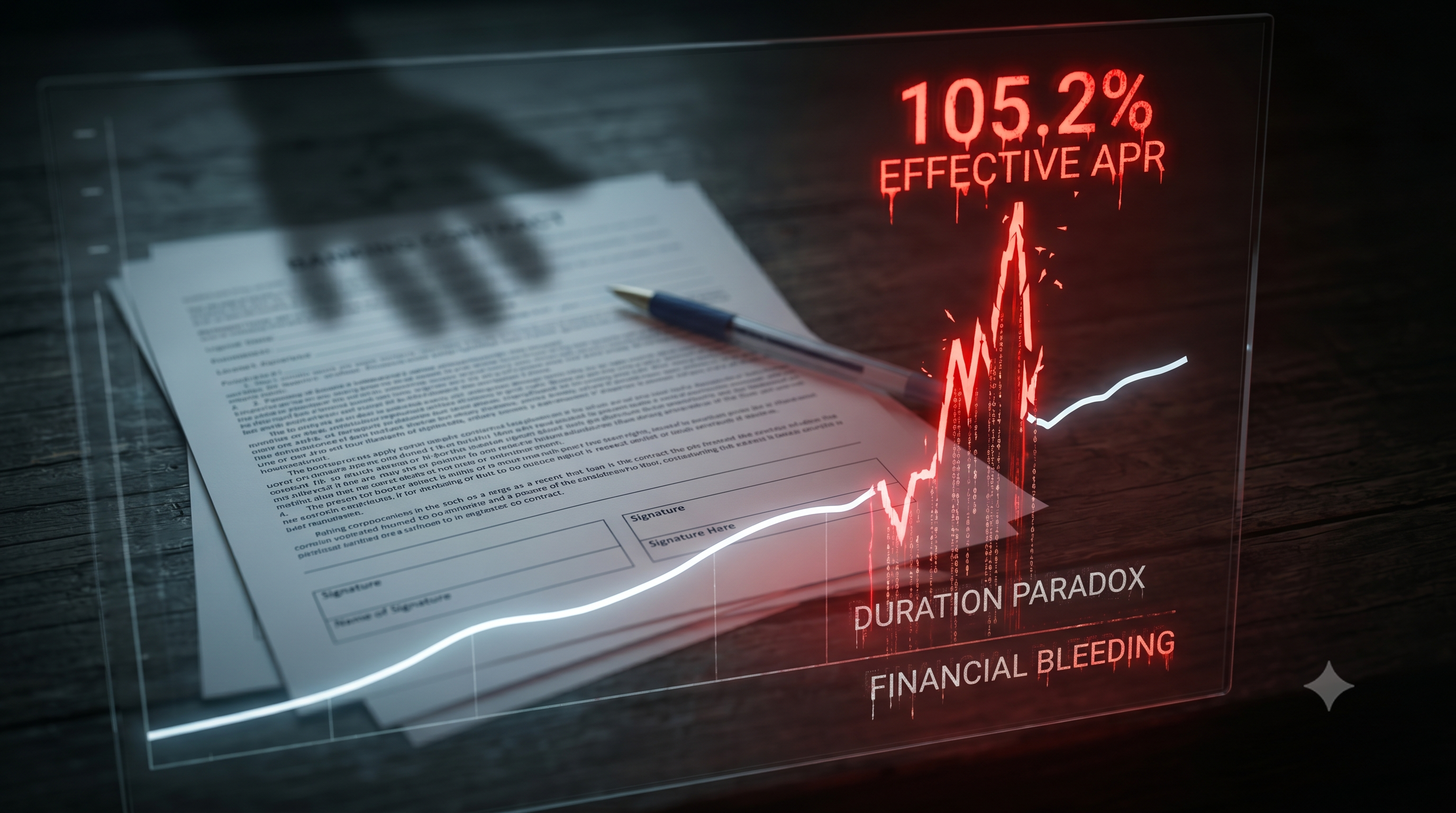

Listen to me very carefully: MCAs are not a safety net; they are mathematically designed to punish your success through a toxic little trap known as a "duration paradox." Just know up front that we will help the few businesses that can benefit from strategic MCA’s. But let’s look at the numbers as to why we need to be very cautious…

Because an MCA uses a fixed factor rate instead of a traditional interest rate, paying the advance off faster actually exponentially increases your effective APR. Let's say you take an MCA, use the cash, crush your marketing goals, and scale rapidly enough to pay the whole thing off in 90 days. Congratulations, you just spiked your effective APR to an astronomical 105.2%.

And that’s if you’re lucky. At the extreme end, MCA effective APRs routinely exceed 350%. 📉💸

You took an advance to survive, and the lender mathematically penalized you for actually growing your business fast. Traditional finance isn't designed to help you scale; it's designed to bleed you.

Don't fall for the trap.

Manufacturing Your Own Float: The Funding Machine

So, how do you actually apply this right now? You aren’t Jeff Bezos, and you can’t just ruthlessly hold your vendor's cash hostage for 98 days. You also can't magically force your corporate B2B clients to pay your invoices two months early.

But you can engineer your own institutional float today. You do it by utilizing the ultimate financial cheat code: 0% introductory business credit facilities. 💳

This is your personal GEICO. By securing up to $300,000 in 0% capital, you instantly create a massive, revolving float of Other People’s Money. Instead of burning your own hard-earned cash to fund payroll, inventory, and marketing while you wait for those suffocating 45-day invoices to finally clear, you deploy the bank's money. You scale operations, acquire new clients, and generate fresh revenue - all before you ever have to pay a single dime of interest.

And the absolute best part? The tax and legal shields are completely bulletproof. 🛡️

When you pull capital from these credit facilities, it is entirely tax-free. The IRS can’t touch it because it’s legally offset by a liability. Furthermore, unutilized business credit is virtually invisible. If a predatory lawyer looks at your balance sheet looking for an easy lawsuit, you look completely flat broke. But in reality, you are sitting on the purchasing power of a giant. It is the ultimate unfair advantage.

Stop Playing Defense

It is time to completely rewrite your financial playbook. Stop acting like a scared retail consumer trying to save your way to wealth, and stop being an involuntary, zero-interest lender to your own clients.

You cannot build a massive empire by playing defense and waiting for permission to get paid. You build it by mastering capital velocity, securing free money, and forcing the system to work for you.

Plug directly into the Funding Machine. Secure the exact 0% capital facilities that the traditional banks are desperately trying to keep hidden from you. Reverse your cash flow cycle, build your float, and start playing the wealth game exactly like the elite do.

Let's get you funded. LFG! 🚀